Financial abuse had shaped many homes before family members, friends, or advocates had a clear name for it. Money, debt, work, banking access, credit, transportation, and financial records had become ways one person controlled another person’s choices. For many survivors, safety had not only meant leaving harm; it had also meant finding rent, food, childcare, phone access, healthcare, legal support, wages, documents, and a path back to stability.

FreeFrom had helped bring this reality into public view by centering survivor financial security before, during, and after crisis. Its work described financial insecurity as the number one obstacle to safety for survivors. In that shared story, financial abuse help became part of housing, work, credit recovery, family safety, and long-term healing.

In this article

- How Financial Abuse Changed Daily Life

- Why Financial Abuse Made Money a Safety Issue

- How Survivors Prepared With Support

- How Financial Abuse Help Supported Recovery

The story often began in ordinary language. A partner may have said that he would manage the bills, watch the budget, handle banking, or decide when work and transportation made sense. Over time, those choices could become limits, and a survivor’s connection to income, savings, documents, and trusted friends could grow smaller.

Families and close friends often noticed strain before they understood the pattern. A missed shift, a lost phone, a blocked account, an unpaid bill, or sudden transportation trouble could seem separate at first. Together, those moments showed how financial control could affect safety, housing, work, childcare, and recovery long after the relationship had changed.

How Survivors Found Financial Abuse Help and Safety

Financial abuse had reached beyond money because money touched nearly every part of daily safety. It affected where someone slept, whether children reached school, whether a phone stayed connected, whether work continued, and whether a survivor could meet an advocate or trusted friend. When communities understood that pattern, financial abuse help became central to survivor support.

How Financial Abuse Changed Daily Life

Financial abuse was a pattern of control involving money, work, debt, credit, banking access, transportation, and financial information. It often appeared within coercive control, where one person gradually limited another person’s ability to make safe decisions. In many households, the harm had grown slowly through withheld information, monitored choices, and restricted access.

The signs could include taking paychecks, blocking employment, restricting bank accounts, monitoring purchases, forcing debt, opening accounts without consent, hiding financial records, refusing transportation, damaging credit, or withholding money for necessities. A partner may have first appeared helpful while taking over household finances. Later, the survivor may have found that income, records, work, transportation, and savings were no longer easy to reach.

This abuse could continue after separation. Shared debt, unpaid bills, coerced loans, identity misuse, court costs, and damaged credit could follow survivors for years. Those harms could affect housing applications, utility accounts, employment, childcare, healthcare, transportation, and long-term safety.

FreeFrom’s work treated economic abuse as a core part of domestic violence, not a side issue. Its resources described economic abuse as a tactic that could include unsafe bank access, being prevented from working, or debt placed in a survivor’s name without that survivor’s knowledge. That recognition mattered because many survivors had not identified the abuse right away when it had been framed as budgeting, concern, management, or protection.

Why Financial Abuse Made Money a Safety Issue

Leaving abuse had often created immediate costs. Survivors may have needed emergency housing, food, transportation, childcare, legal support, replacement identification documents, medical care, a secure phone, or internet access. When income, accounts, credit, or transportation had been controlled, those ordinary needs became serious barriers.

FreeFrom’s supplied figures said survivors reported needing an average of $1,567 to make ends meet and stay safe. At the same time, survivors reported having only $10 in savings and less than $300 that they alone could access. That gap showed why flexible financial support had mattered so much in real homes and communities.

Safety could depend on a security deposit, car repair, phone bill, hotel room, groceries, childcare, or transportation to court. A rigid aid program may not have matched the expense that mattered first. Flexible support respected the survivor’s knowledge of the household, the children, the commute, the risk, and the next safer step.

Employment disruption often made the barrier larger. Some survivors had been prevented from working, while others lost income because of stalking, harassment, transportation limits, missed shifts, childcare instability, or interference from an abusive partner. FreeFrom’s policy work connected survivor financial security with safe work, stable income, and protections against retaliation or job loss.

Housing added more pressure. Rental applications, utility accounts, mortgages, and loans often depended on credit history and steady income. Survivors with coerced debt, identity misuse, unpaid shared bills, or damaged credit could face more barriers while trying to build independent housing and safety.

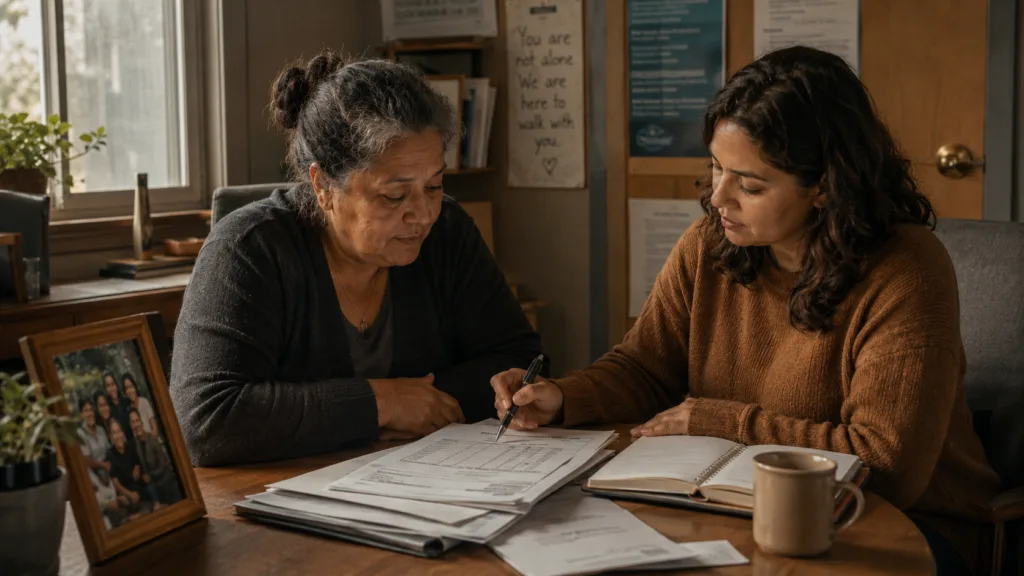

How Survivors Prepared With Support

Financial preparation had to be handled carefully when a partner monitored phones, accounts, email, devices, banking apps, location data, or mail. Many domestic violence organizations recommended speaking with an advocate before major financial or legal changes. That support mattered because one helpful step in one home could create risk in another.

A financial safety plan could include creating a private email account, changing passwords, gathering identification documents, saving copies of records, reviewing account access, documenting debts, checking credit reports, and opening a separate account only when safe. Important records could include a driver’s license, passport, Social Security card, birth certificates, immigration documents, insurance cards, pay stubs, tax records, court papers, lease agreements, bank statements, loan records, and benefit information. Each document could become part of a survivor’s path toward housing, work, benefits, childcare, and legal support.

Technology safety had become part of financial safety. Shared devices, cloud accounts, phone plans, GPS tracking, payment apps, and banking notifications could expose private activity. A survivor may have needed a safer device, trusted mailing address, or advocate’s help before changing passwords or account settings.

Credit and debt review could also reveal hidden harm. Financial abuse may have involved coerced loans, unauthorized credit cards, unpaid bills, utility accounts, medical debt, or identity misuse. Reviewing credit reports could help identify unfamiliar accounts, collections, late payments, or debts that needed documentation.

Recovery often unfolded in stages. Immediate steps may have focused on safety, food, housing, transportation, and basic needs. Later steps may have included savings, credit repair, stable work, coerced debt support, benefits, housing, and legal guidance with advocates and trusted community members.

How Financial Abuse Help Supported Recovery

Survivors often needed several kinds of support at once. Confidential safety planning, emergency cash, housing help, transportation, childcare, legal aid, credit counseling, employment support, savings tools, and financial education could all belong to the same recovery story. A clear resource path helped families, friends, and advocates move from recognition toward steady support.

FreeFrom provided survivor-focused resources built around financial security. Its Safety Fund offered flexible, no-strings-attached cash assistance that survivors could use for needs such as rent, utilities, car expenses, healing resources, or other safety-related costs. That flexibility reflected what many advocates had seen: the survivor closest to the risk often knew which expense mattered first.

FreeFrom’s Savings Matching Program helped survivors build emergency savings by matching savings dollar for dollar up to $55 per month. The program also included a $120 bonus, for up to $1,440 over a year. Its survivor resources included community financial coaching, a 12-week financial knowledge program, and an online Resource Hub for financial stability.

The supplied material also noted that being a survivor costs an average of $104,000 in medical costs and lost productivity over a lifetime. That figure showed why short-term crisis help had not been enough for many households. Long after the first safety decision, survivors and families may still have faced damaged credit, lost income, housing barriers, healthcare costs, employment disruption, and debt.

National resources could stand beside local and survivor-centered help. The National Domestic Violence Hotline offered confidential support, safety planning, and referrals for people experiencing abuse. The National Network to End Domestic Violence provided economic justice resources focused on survivor financial safety and policy, while the Consumer Financial Protection Bureau offered tools related to debt, credit, banking, and financial recovery.

FAQs

Financial abuse was control over money, work, debt, credit, bank accounts, transportation, housing, or documents. It could include taking income, blocking work, limiting account access, creating debt, hiding records, or controlling basic needs.

Signs could include monitored spending, missing documents, blocked accounts, restricted transportation, unpaid shared bills, taken paychecks, forced debt, or pressure to sign financial agreements. Friends and family may have noticed stress around money before the larger pattern was clear.

Money affected housing, food, transportation, childcare, healthcare, legal help, phone access, and emergency plans. When an abusive partner had controlled income or credit, leaving could create new risks without flexible support.

FreeFrom focused on survivor financial security through flexible cash assistance, savings support, financial education, coaching, compensation guidance, research, and policy advocacy. Its work treated economic abuse as a central safety issue.

Help could include emergency cash, housing support, transportation help, childcare assistance, legal aid, credit counseling, employment support, matched savings, benefits navigation, and financial coaching. Local domestic violence programs and national hotlines could connect survivors with available resources.

Advocates helped survivors think through safety when phones, email, accounts, devices, location data, or mail may have been monitored. Their guidance could make financial steps safer, quieter, and more private.

How Financial Abuse Help Supported Long-Term Safety

FreeFrom’s survivor resources remained a steady place where financial abuse recovery tools, education, savings support, and survivor-centered assistance could be found.

More on FreeFrom

Explore FreeFrom from every angle: