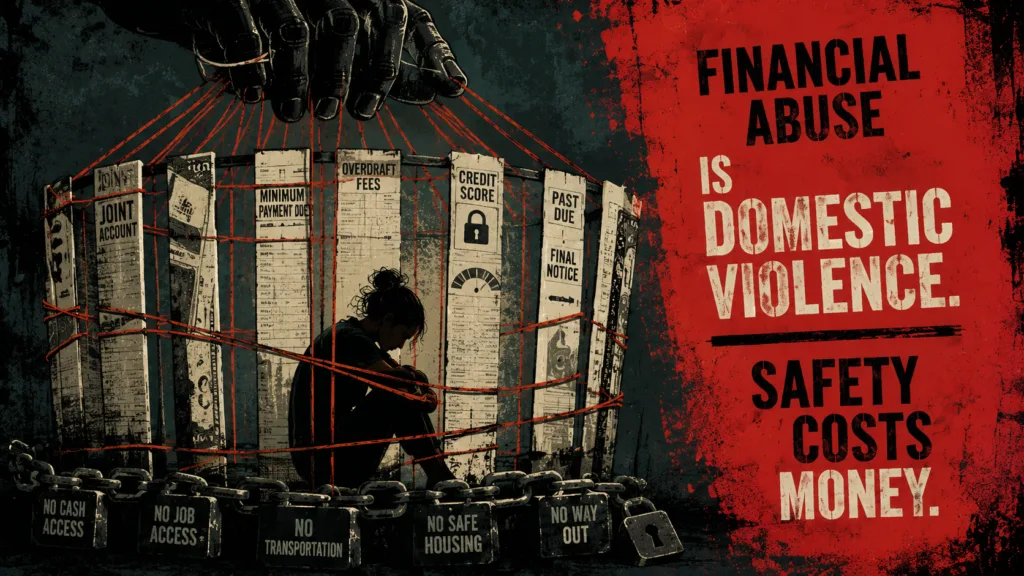

You cannot treat financial abuse like a side problem. That mistake is dangerous, and survivors pay for it with housing, work, transportation, credit, healthcare, and safety. When someone controls your money, accounts, documents, debt, or job access, they control the exits. Financial abuse help matters because safety costs money.

Financial abuse is domestic violence. They use money to trap people, isolate them, punish them, and make leaving feel impossible. FreeFrom names financial insecurity as the number one obstacle to survivor safety. That should make every crisis-only response look weak.

In this article

- What financial abuse looks like.

- Why lack of money keeps survivors trapped.

- How to plan for financial safety.

- Where survivors can get help.

You need clear language because abuse hides behind confusion. Financial abuse can look like budgeting, concern, protection, or household management until it becomes control. Then your paycheck, bank access, documents, transportation, phone, housing, and credit sit under someone else’s grip. That is not care; that is control.

Leaving abuse is not only a safety decision. It is also a financial decision. Rent, food, childcare, legal costs, missed wages, phone access, healthcare, and damaged credit can decide what happens next. Financial abuse help must face that reality without softening it.

Financial Abuse Help

Financial abuse is a pattern of control involving money, work, debt, credit, banking access, transportation, and financial information. They do not need visible injuries to create fear. They can take your paycheck, block your job, hide accounts, force debt, damage credit, or hold documents hostage. The result is fewer choices and more danger.

Survivors need support before, during, and after crisis. Immediate safety matters, but long-term financial recovery matters too. Abuse can follow survivors through unpaid bills, coerced loans, court costs, identity misuse, collections, and damaged credit. That harm does not stop because someone leaves.

What financial abuse looks like.

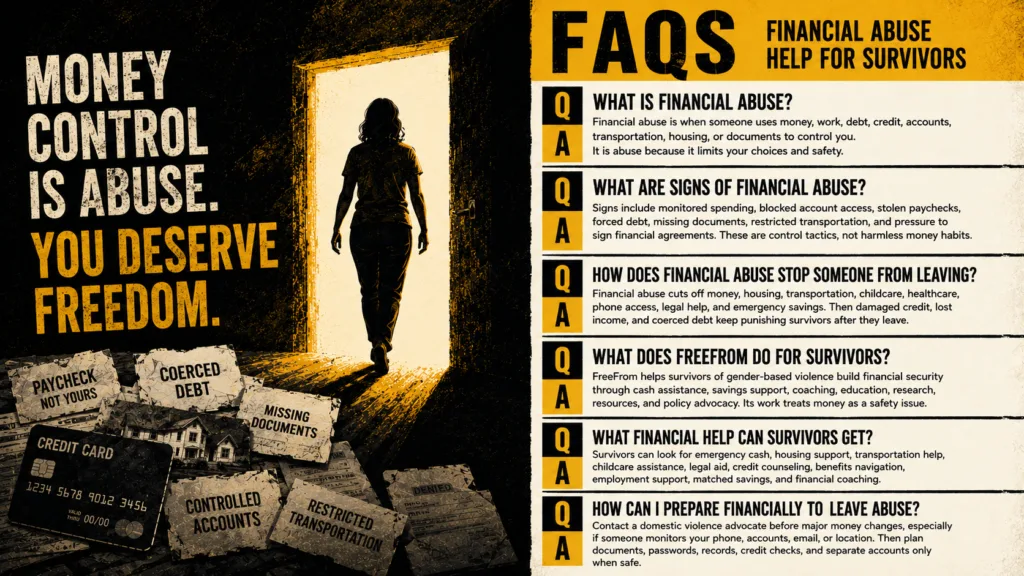

Financial abuse happens when someone uses money, employment, banking, debt, credit, housing, documents, or dependence to control your life. It can start quietly. They may offer to handle finances, then restrict access, monitor spending, block work, hide information, or decide what necessities you get. The pattern becomes clear once you name it.

Warning signs include needing permission to spend, losing access to income, missing financial records, locked accounts, unpaid shared bills, and debt in your name. They may track purchases, take paychecks, pressure you to sign agreements, restrict transportation, or refuse money for basic needs. That is not normal conflict. It is control built to keep you anxious and dependent.

Financial abuse can continue after separation. Shared debt, coerced loans, damaged credit, court costs, unpaid utilities, and identity misuse can follow survivors for years. They can affect housing applications, job stability, childcare, healthcare, transportation, and basic independence. This is why financial abuse help cannot stop at “just leave.”

Many survivors do not identify financial abuse right away because the behavior wears a disguise. They call it budgeting, protection, responsibility, or concern. Over time, that disguise turns into isolation and fear. People need language that exposes the pattern before the trap gets tighter.

Economic abuse is not a side issue in domestic violence. FreeFrom’s work treats unsafe bank access, blocked employment, and hidden survivor debt as central abuse tactics. That matters because people cannot escape what nobody will name. Financial abuse help starts with refusing to sanitize the control.

Why lack of money keeps survivors trapped.

Leaving abuse creates immediate costs. You may need emergency housing, food, transportation, childcare, legal help, replacement documents, medical care, phone access, or internet access. Those needs are not extras. They are the difference between a safer exit and another forced compromise.

Survivors report needing an average of $1,567 to make ends meet and stay safe. They may have only $10 in savings and less than $300 they alone can access. That gap is brutal, and it exposes why “just leave” is such a reckless phrase. Safety becomes harder when the money needed for safety sits out of reach.

Flexible financial support matters because survivors do not all need the same expense solved first. One person needs a security deposit. Another needs a car repair, hotel room, phone bill, groceries, childcare, or transportation to court. Rigid aid programs fail when they treat survival like a neat checklist.

Employment disruption makes the trap worse. They may prevent work, sabotage shifts, stalk workplaces, restrict transportation, or create childcare instability. Lost income then becomes another weapon. Survivor financial security needs safe work, stable income, and protection from retaliation or job loss.

Housing adds another pressure point. Rental applications, utilities, mortgages, and loans depend on credit and income. Coerced debt, identity misuse, unpaid shared bills, and damaged credit can block independent housing. Financial abuse help must include credit recovery, cash support, and long-term stability.

This is why survivor-centered support must respect autonomy. They cannot assume every survivor needs the same answer. A survivor knows which expense creates the worst danger right now. Aid that ignores that reality becomes another gate.

How to plan for financial safety.

Financial preparation needs caution when someone monitors phones, email, devices, accounts, banking apps, mail, or location. A rushed move can create danger. A domestic violence advocate can help you plan without alerting the person watching you. Safety planning is not paranoia; it is strategy under pressure.

A financial safety plan may include a private email account, stronger passwords, copies of records, identification documents, and a review of account access. Important records can include a driver’s license, passport, Social Security card, birth certificates, immigration documents, insurance cards, pay stubs, tax records, court papers, lease agreements, bank statements, loan records, and benefit information. You deserve access to your own life on paper. Anyone blocking that access knows exactly what they are doing.

Technology safety now belongs inside financial safety. Shared devices, cloud accounts, phone plans, GPS tracking, payment apps, and banking notifications can expose private activity. You may need a safer device, trusted mailing address, or advocate support before changing passwords. Digital trails can become real-world danger.

Credit and debt review can show damage they tried to hide. Coerced loans, unauthorized cards, unpaid bills, utility accounts, medical debt, and identity misuse can all appear in credit reports. Checking reports can reveal unfamiliar accounts, collections, late payments, or debt that needs documentation. Evidence matters when the financial harm follows you.

Recovery happens in stages, not one heroic leap. First comes safety and basic access. Then come savings, credit repair, stable work, debt documentation, benefits, housing, and legal support. FreeFrom’s survivor programs reflect that reality through flexible cash assistance, savings support, financial coaching, financial education, and an online Resource Hub.

Financial safety planning should never punish a survivor for moving carefully. The danger is real when accounts, phones, passwords, and location data expose private choices. Survivors may need time, tools, and confidential support before taking visible action. Smart planning protects people from systems and abusers that punish every mistake.

Where survivors can get help.

Survivors may need confidential safety planning, emergency cash, housing help, transportation, childcare, legal aid, credit counseling, employment support, savings tools, and financial education at the same time. That is not disorganization. That is what abuse breaks. Resource lists must move people from recognition to action without dumping more overwhelm on them.

FreeFrom focuses on survivor financial security because crisis response alone is not enough. Its Safety Fund offers flexible, no-strings-attached cash assistance for survivor-defined needs. That can include rent, utilities, car expenses, healing resources, and other safety-related costs. Flexible cash respects the person living the danger.

FreeFrom’s Savings Matching Program helps survivors build emergency savings. It matches savings dollar for dollar up to $55 per month, adds a $120 bonus, and can provide up to $1,440 over a year. That support matters because stability takes time. A single emergency payment cannot repair years of controlled income, debt, and blocked options.

Being a survivor costs an average of $104,000 in medical costs and lost productivity over a lifetime. That number should make shallow support models look disgraceful. Survivors need more than sympathy after violence wrecks income, health, housing, and work. They need material support that treats financial recovery as safety work.

National resources also matter. The National Domestic Violence Hotline provides confidential support and safety planning. The Consumer Financial Protection Bureau offers tools on debt, credit, banking, and recovery. The National Network to End Domestic Violence addresses economic justice and survivor financial safety. These resources exist because money abuse is real abuse.

Resources should not make survivors prove pain before they get help. They should not bury people in forms while rent, transportation, food, and phone access become urgent. Financial abuse help has to move money, information, and power toward the person facing danger. Anything less keeps the cage standing.

FAQs

Financial abuse is when someone uses money, work, debt, credit, accounts, transportation, housing, or documents to control you. It is abuse because it limits your choices and safety.

Signs include monitored spending, blocked account access, stolen paychecks, forced debt, missing documents, restricted transportation, and pressure to sign financial agreements. These are control tactics, not harmless money habits.

Financial abuse cuts off money, housing, transportation, childcare, healthcare, phone access, legal help, and emergency savings. Then damaged credit, lost income, and coerced debt keep punishing survivors after they leave.

FreeFrom helps survivors of gender-based violence build financial security through cash assistance, savings support, coaching, education, research, resources, and policy advocacy. Its work treats money as a safety issue.

Survivors can look for emergency cash, housing support, transportation help, childcare assistance, legal aid, credit counseling, benefits navigation, employment support, matched savings, and financial coaching.

Contact a domestic violence advocate before major money changes, especially if someone monitors your phone, accounts, email, or location. Then plan documents, passwords, records, credit checks, and separate accounts only when safe.

Financial Abuse Help Means Real Safety

Use FreeFrom’s survivor resources because financial abuse help should protect your choices, not leave you trapped in someone else’s control.

- FreeFrom Survivor Resources — Financial support programs, savings tools, coaching, and survivor-centered resources.

- FreeFrom Get Involved — Donate, shop at Gifted, advocate, connect.

- National Domestic Violence Hotline — Confidential support, safety planning, and referrals for people experiencing abuse.

- National Network to End Domestic Violence: Economic Justice — Information on economic abuse, financial safety, and survivor-centered policy issues.

More on FreeFrom

Explore FreeFrom from every angle: